10- Bitcoin’s use cases

Have you bought your first SATs? Well, then: welcome; you are now part of one of the greatest revolutions in human history. You just made your first step, and you “got off zero”. Rejoice.

Now…what? What happens now that you acquired some Bitcoin? What’s the best approach: should you accumulate it, spend it, or both? Should you “set and forget” it?

Well, I can’t really tell you. Your money, your choice.

However, I feel like it’s my duty to at least talk you through the vast realm of possibilities Bitcoin offers.

Unlike what the fiat guys love to say, there are many ways for you to make use of your SATs.

“You can’t live in a Bitcoin”. Haters, and more specifically real estate investors, revel in such nonsense.

We are about to prove them wrong, big time, while also maintaining a healthy level of realistic expectations.

Fast, worldwide payments with no intermediaries.

First, let’s address the elephant in the room.

Has Bitcoin failed as a currency and a medium of exchange? Is Bitcoin the best money that never was?

You don’t have to be a financial analyst to see that prices are still 99.99% denominated in fiat, and that very few merchants accept Bitcoin in exchange for their products.

“A purely peer to peer version of electronic cash (that) would allow payments to be sent from one party to another“.

Remember? This is the opening line from the 2009 whitepaper, written by Satoshi. This single quote is a testament to his original vision: Bitcoin as a global, permissionless, and independent digital payment system.

Does that mean his dream has gone astray? Has Satoshi’s original project been “betrayed”? Well, no, it hasn’t. I would argue that it only changed direction, for now;

only to rise, in the future, as the new monetary standard, once the world fully realizes just how valuable it is.

Bitcoin is an incredibly efficient and fast payment system: one that knows no borders or restrictions.

Nonetheless, this was Bitcoin’s intended main “use case”. A system that operates outside of the traditional finance apparatus, and that enables two parties to instantly settle payments, no matter where in the world they are.

The blockchain records more than half a million transactions per day, which is nothing compared to giants such as Visa or Mastercard, but remember: many people who use Bitcoin do it because they “have to”, as they have no access to the banking system.

Let’s take a moment to appreciate just how important this is. Thanks to Bitcoin, everyone with an internet connection can instantly send and receive value.

Sending remittances to your family has never been easier. No more offices, paperwork, high fees, stupid conversion rates, long waits.

Just ask your Dad for his Bitcoin address, paste it, and press “send”. Done. In minutes, the money travels across the world and it’s (nearly) instantly received. Easy.

Let’s add Bitcoin’s “uncensorability” and high grade of privacy, and we can see just why it is such an impressive product. Don’t forget: no one is capable of “stopping” Bitcoin. No one can prevent you from using it, not even your government. No wonder Bitcoin is often referred to as “freedom money”.

The new gold?

Ok, I hear you. Maybe you live in a western country, or in a well-developed nation, and you feel like you don’t really need to rely on Bitcoin for payments.

You can “Venmo” your friend. You can send fast bank transfers using fiat money. Fair enough.

You may see Bitcoin as “too valuable” to be used as a medium of exchange: those $200 you owe your friend? Why would I spend Bitcoin, when I know it’s going to exponentially increase in value?

Why would I get rid of it, instead of accumulating it for my happy retirement? I don’t want to spend it! It’s like my precious gold coin: I’ll just keep it for the years to come, rather than selling it now.

If that’s your line of thought, let me tell you: you are not alone!

That is, in fact, what the vast majority of Bitcoin holders think.

And let me reiterate what I said in an earlier chapter: there is no right or wrong way to use Bitcoin; it entirely depends on your needs, your views, and your living conditions.

And so, do not be afraid, if your only “use case” is to hoard it and watch it grow, until the day it can buy you a house. It’s ok! Don’t let purists tell you what to do with your money.

You could have bough your future home for only $500. You are still in time.

As of today, “store of value” is Bitcoin’s main use case. Not “day-to-day” currency but “safe haven”.

As you learned before, this role has historically belonged to gold: the king of money.

We don’t need to repeat what we already know, but as a reminder, the precious metal has been so widely successful because of its unparalleled qualities such as: scarcity, portability, divisibility and, broadly speaking, value.

We also know that Bitcoin outperforms gold in every way, and it’s just a matter of time before everyone finds out. Not just yet, though: Bitcoin’s market cap is still more than 10 times smaller, compared to the yellow metal.

But the tides are turning, and BTC is on its way to dethrone, in the years to come, gold as the perfect store of value. Indeed, just look at the numbers: one Bitcoin was literally worthless only 15 years ago, while it now costs more than $100,000, and saw its value increasing more than 1 million percent.

Governments adore gold, and they love to accumulate it in vaults and reserves.

Now, it’s time for Bitcoin to shine.

Countries are taking their first steps towards adopting BTC as a “reserve asset”, and things are going to escalate quickly, mark my words.

In a not-so-distant future, I am betting the global money system will likely be backed by Bitcoin, just like we saw happen with the “gold standard” in the past. It’s not sci-fi, but a concrete possibility.

This is, in my opinion, why Bitcoin has so far disappointed as a currency. It’s so valuable that people would rather keep it, instead of spending it.

So, what does this mean for you, as a long term HODLER? Are you just going to sit on your stack, guarding it without ever using it? Are you going to take your money to the grave with you?

What if I told you there is a way to perfectly combine your multi-year commitment with the enjoyment of “selling” Bitcoin, without actually doing it?

Your very own fiat printing machine

Did I just claim you can taste your pie without eating it? Yessir, I very much did.

And this may actually be Bitcoin’s greatest use case, depending on who you ask. This is not something Satoshi envisioned, I believe. But since Bitcoin became more and more “institutionalized” and “financialized”, this new thing emerged as one of the best ways for you to make your stack productive without ever having to sell it.

What am I talking about?

Well, not only is Bitcoin the best store of value around; it’s also the very best collateral available. Hear me out and, although this may not interest you just yet, especially as a total beginner, just know that this amazing possibility is out there!

If you ever tried to borrow money from a bank, you know how painful the process can get. Unless you are rich or well-off, of course.

For the average person, the odds of getting a loan are very slim. That’s because nobody will lend you a penny unless you can prove you are 100% able to repay your debt—and, to be fair, that makes perfect sense.

See? I’m on the bank’s side, for once!

A financial institution will happily give you cash only if you can put a valid collateral on the table, or anything that proves you are financially stable. This can be any item which value matches the loan you are requesting.

If you wish to borrow 10,000$, you could use your car as a collateral, as long as it is valued at around 10k or more. That way, if you are not able to repay your loan, the bank will seize the asset and sell it, thus ensuring they have not lost money on you.

Other forms of collateral could be your house, your land, your jewellery. Anything that has value, basically.

Now, it doesn’t take a genius to figure out that for a working class person, this is just unattainable. The majority of us can never access a loan.

But even if they could, the whole thing is complex, lengthy, and uncertain.

Your collateral must be carefully evaluated by some rating agency, and you need to go through meetings, phone calls, credit checks, provide tons of documents, proof of income and whatnot. It’s just a pain in the arse, as they would say in the UK.

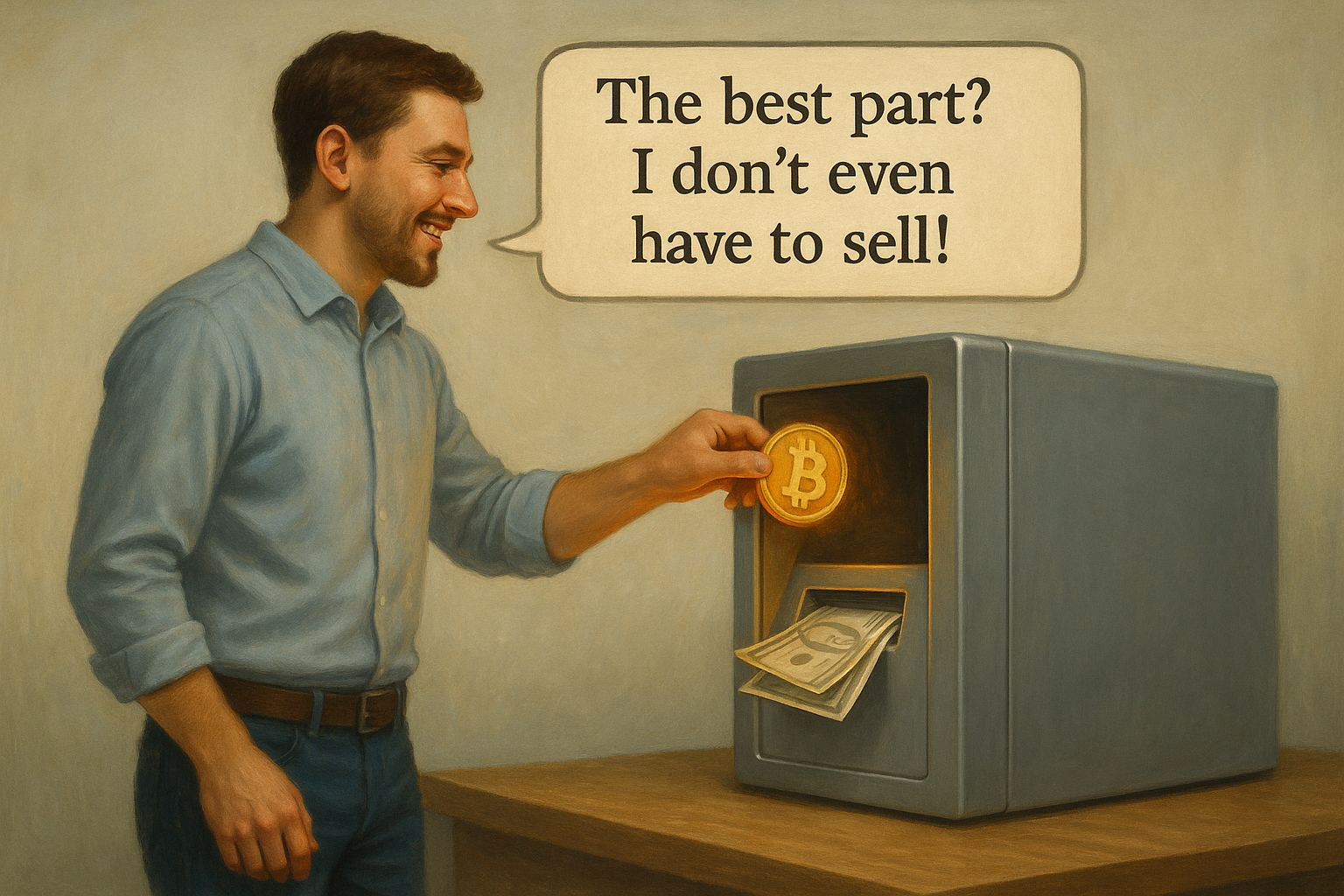

Grow your stack, borrow against it, make money. Repeat, and get rich.

Enter Bitcoin: the best collateral ever. This deserves a dedicated chapter and there is a lot to say, but we will try to keep it short, for now.

In essence: once you have a decent amount, you can literally turn it into a fiat printing machine. Yes, you can generate money without selling any of your Bitcoin, granted you are smart about it.

There are companies who operate internationally, such as Ledn, just to name the biggest one, who will give you fiat loans if you are willing to use your Bitcoin as a collateral.

No questions asked, no credit checks, no meetings, no nothing. Just send the matching amount of BTC to their address and, in a matter of hours, you will receive the money in your bank account.

The more I think about it, the more genius it seems.

Think about the endless possibilities this opens up, for the average person. Now, people in poorer countries, granted they are able to repay their debt, can access instant liquidity without headaches.

Have you always dreamed about opening a tiny business, or a small start-up? Well, now you can. You are able to borrow and obtain money in less than a day. and get started.

We talked about how rich people manage to stay rich. Remember? They are not saving in fiat. They stack assets and then, crucially, they borrow against them. This gives them the ability to “print” money without parting ways with their valuable assets. Now, you can do the same. Are you not excited?

Why is Bitcoin the best form of collateral? It’s easy, really. It can be sent and resold at instant speed. Companies such as Ledn are not worried about anything.

In case you fail to repay your debt, they can simply keep the Bitcoin you sent as a collateral. No worries. If they need liquidity, they can immediately sell it, and they won’t have lost any money. This is light years ahead, compared to the traditional system, where your collateral must be examined very carefully.

Once you repay your fiat debt, your Bitcoin will be returned to you: your stack is still intact, while you just funded your first small business: life’s good.

But wait, hold your horses. This doesn’t come without risks. If you intend to go this route, please do your homework, and consider every possibility. Things can go wrong, very wrong, in fact.

If Bitcoin’s price crashes and you receive the dreaded “margin call”, will you be able to cope with it, or will you get liquidated?

You see, with Bitcoin lending, you must always keep a delicate balance between the value of your collateral and the one of the loan you requested.

It’s called “loan to value” ratio, and in short, it implies that, if you borrowed $100, you must send at least $200 worth of Bitcoin.

But as we know, Bitcoin’s price can wildly swing without warning. And if that ratio goes out of whack, and you are not able to “top up” your collateral, that’s game over. You are getting liquidated, and you can say adios to your Bitcoin.

Moreover, you must be careful, when trusting your Bitcoin to a financial institution. Make sure the company you choose has a proven track record, and that it’s worth your trust. If they go bankrupt, that’s also game over.

Just play it safe, and you will be fine. Again, this is an amazing way for you to make your dreams come true. No need to sell your Bitcoin, no need to pay an absurd amount of taxes. Borrow against it. That’s the way.

How to actually spend your Bitcoin

But what happens, when everyone just accumulates Bitcoin without ever using it? Will the ecosystem slowly die, will it disappear?

No one knows the answer, but some hardcore Bitcoiners think it will.

Jack Dorsey, a prominent member of the community and Twitter Co founder, recently warned us: if BTC fails to become an actual currency, it will slowly fall into irrelevance, and die.

The theory has its merits and, depending on how you see it, it could be accurate, or just completely wrong; after all, if Bitcoin rose from $0 to 100 000$ without becoming a relevant form of money, why would it fail now? We are not here to debate, however, so let’s just examine it.

Jack, together with many others, is a proponent of the “spend and replace” method: use your Bitcoin as much as you can in your daily life, so that the system keeps growing, and the network keeps expanding. This is likely akin to Satoshi’s original vision: Bitcoin as a real medium of exchange and a currency.

The method is fairly simple, and although not entirely beginner-friendly, it can actually be implemented by anyone: use Bitcoin instead of fiat, where you can, and immediately replace the SATs you just spent with new ones, so that the total value of your stack always stays the same.

Let's say you want to purchase a new laptop that costs $1000: instead of buying it with Dollars, you can purchase it using Bitcoin (0.001BTC, for example).

The next step is to simply buy 0.001 Bitcoin with fiat to replenish your holdings.

This ensures that the amount of worldwide Bitcoin payments increases, while also encouraging more merchants to start accepting it as a form of payment.

The theory is legitimate and it works, but it sure requires some extra work, calculations, and know-how.

But people are lazy, that includes me, and I wonder if this will ever take off.

You are now wondering how to actually buy a laptop with Bitcoin, aren't you?

You can realistically replace fiat with Bitcoin for nearly all of your daily needs.

There are many ways for you to spend your SATs on everyday items, I guarantee.

It may be a little obscure and less obvious, but if you know where to look, you can actually start living in your “Bitcoin standard”.

The easy one: look for merchants that accept Bitcoin—yes, they do exist.

Whether it’s an online retailer (mostly tech) or a physical shop, such as a café or a restaurant, the amount of businesses that also trade in BTC is growing everyday.

For four years I lived in a semi-remote, tiny town in northern Australia, where at least three restaurants accepted Bitcoin payments. I am sure that if you live in a big city, you’ll find plenty.

You won’t see it advertised on their homepages, but you can indeed purchase goods from big names, directly or indirectly, with Bitcoin. You must use back-doors, third parties, other services; but it works. Take a look.

Notable names include:

Tesla

Amazon

Spotify

Microsoft (Xbox services)

Twitch

Overstock.com

Newegg

Express VPN

Starbucks

Whole foods

Subway

Tesco

Coles and Woolworths (Australia)

Walmart

Target

Aldi

Carrefour

Spar supermarkets (in certain countries)

Travala

Cheap air

I am serious. You can theoretically buy all of your groceries, and pay your bills with Bitcoin.

Platforms such as Bitrefill allow you to buy vouchers and gift cards with BTC, and redeem them while you shop with any of those retailers. There are many more, of course.

Please note that, depending on the jurisdiction you live in, these things may not apply. Also, keep in mind that, most of the time, spending Bitcoin results in a “taxable event”. Do your research, as per usual.

The superior asset

Now, the next time you hear someone say Bitcoin is utterly useless, you know exactly what to tell them.

Find me another asset that’s so incredibly versatile. I’ll wait.

Bitcoin has plenty of use cases, as you have been shown. And the beauty of it is that you get to choose exactly what to do with it.

Are you someone who must escape hyperinflation? Do you live in a worn-torn country, and have no access to a bank?

Is your family requesting regular payments, but they live on another continent?

You are planning your retirement, where you will live peacefully in your newly bought sea-side home.

Or maybe, you are an aspiring (like I am) small-scale entrepreneur that sadly can’t get a fiat loan.

Do you wish to use a different currency for your daily purchases, one that keeps increasing in value, thus allowing you to live cheaper, and to retain your purchasing power?

Well, my friend; welcome to Bitcoin! As you can see, there is a use case for just about anyone.

What will yours be?

Whatever you choose to do, one thing remains: you must custody your money the right way.

This guide’s ending is drawing near, but the next chapter may as well be the most important one.

Stay with me, as we discuss self-custody, and the various types of wallets available, along with some much-needed safety tips.